Ah, MiCA, that grand European regulation, a beacon of order in the chaotic sea of crypto! Or so the tale is spun. But let us, in the spirit of Dostoevsky, peer beneath the veneer of this bureaucratic masterpiece and uncover the absurdity that lies within. For what is MiCA, if not a grand masquerade, where the masks of European propriety conceal a global carnival of offshore entities?

MiCA Decoded, a 12-article series for Bitcoin.com News, is penned by the triumvirate of LegalBison’s Co-Founding and Managing Directors: Aaron Glauberman, Viktor Juskin, and Sabir Alijev. These modern-day scribes, armed with quills dipped in regulatory ink, guide us through the labyrinth of LegalBison, where crypto and FinTech companies find solace in MiCA licensing, CASP and VASP applications, and the arcane art of regulatory structuring across Europe and beyond.

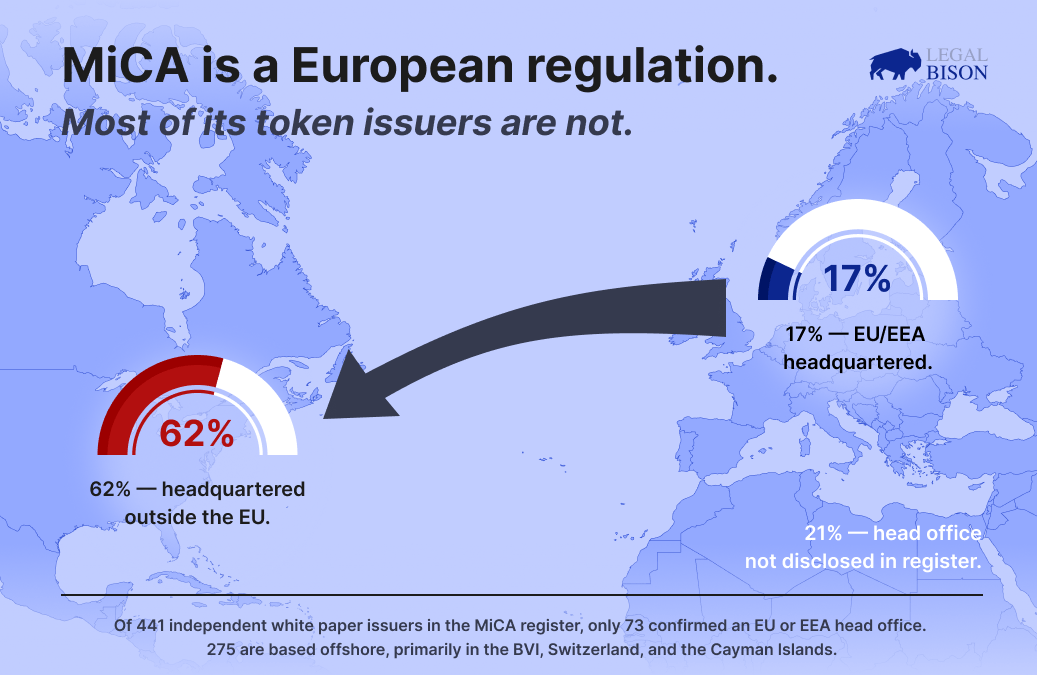

Imagine, if you will, a white paper-that sacred document-filed not from the heart of Europe, but from the sun-drenched shores of the British Virgin Islands or the alpine serenity of Switzerland. For the European Securities and Market Authority (ESMA) public registers reveal a truth as stark as a winter’s dawn: of 441 token project filings in the MiCA registers as of March 12th, 2026, a mere 73 hail from the EU or EEA. The rest? A motley crew of 275 entities, primarily from the British Virgin Islands, Switzerland, and the Cayman Islands. Ah, the irony! A European regulation, yet the players are global, their addresses as exotic as the tokens they trade.

MiCA, in its wisdom, governs not the domicile of companies, but the admission of tokens for trading. A design choice, you say? Or a loophole so grand it could only be crafted by the minds of regulators with a penchant for the absurd. For what does it matter if a token is launched from the BVIs or Panama, so long as it finds its way to the European market? The data speaks, and it whispers of a world where regulatory compliance is but a game, and the players are as diverse as the tokens they peddle.

In this, the second installment of our MiCA Decoded series, we delve into the registry of issued crypto-assets, a treasure trove of revelations. Under MiCA, any entity seeking to offer a crypto-asset to EU investors must publish a compliant white paper. But here lies the rub: the obligation falls not on the issuer, but on the offeror. A distinction as fine as a hair, yet one that opens the floodgates to a world of decentralized projects, where the issuer is but a shadow, and the offeror a phantom.

What the white paper register actually measures

Ah, the white paper register, a ledger of intentions, a mirror to the soul of MiCA. It measures not the purity of European intent, but the global reach of regulatory compliance. For in this world, the issuer is but a creator, and the offeror the true architect of market access. And what of the trading platforms? They, too, play their part, assuming the mantle of responsibility, filing white papers on behalf of tokens they offer to the European masses. Kraken, LCX, and others-they are the gatekeepers, the guardians of compliance, yet they bear the burden of legal risk, should the white paper prove but a mirage.

Strip away the proxy filings, the compliance-provider records, and what remains? A mere 477 records of token projects that engaged directly with national regulators. Of these, only 73 confirm an EU or EEA head office. The rest? Offshore entities, reaching into the European market with a targeted filing, not a corporate relocation. Ah, the beauty of it! A regulation that binds not by geography, but by the mere act of filing.

Ireland and Malta: The Whitepaper Go-To Jurisdictions

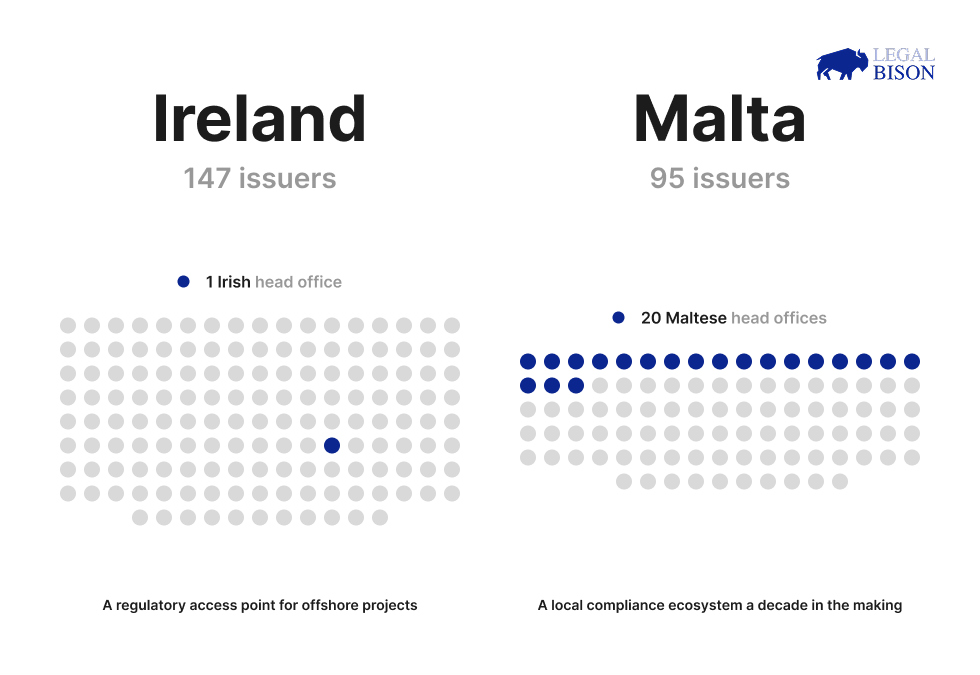

And where do these filings concentrate? In Ireland and Malta, of course, the twin pillars of European regulatory access. Ireland, with its 151 white papers, and Malta, with 145, together account for two-thirds of all independent token project registrations. For the offshore entity seeking a crypto license in Europe, these are the gateways, the portals to regulatory nirvana. Yet, the irony deepens: Ireland, with its English-language process and deep technology sector, is but a filing address, not a corporate home. The British Virgin Islands alone account for 47 of the 116 Irish filers with known head offices. Malta, with its decade of crypto-specific regulation, offers a local ecosystem of compliance professionals, yet only 20 of its 95 entities have a Maltese head office.

The practical difference? It lies in the regulatory environment, the expertise of the regulator, the common law or civil law assumptions that shape their approach. Ireland, with its breadth of filings, from Layer-1 blockchain networks to AI data projects, stands in contrast to Malta, with its fan token platforms and DeFi protocols. Neither shows a category preference, yet each offers a unique path to regulatory compliance.

36 Stablecoins in the EU? How many does the market need?

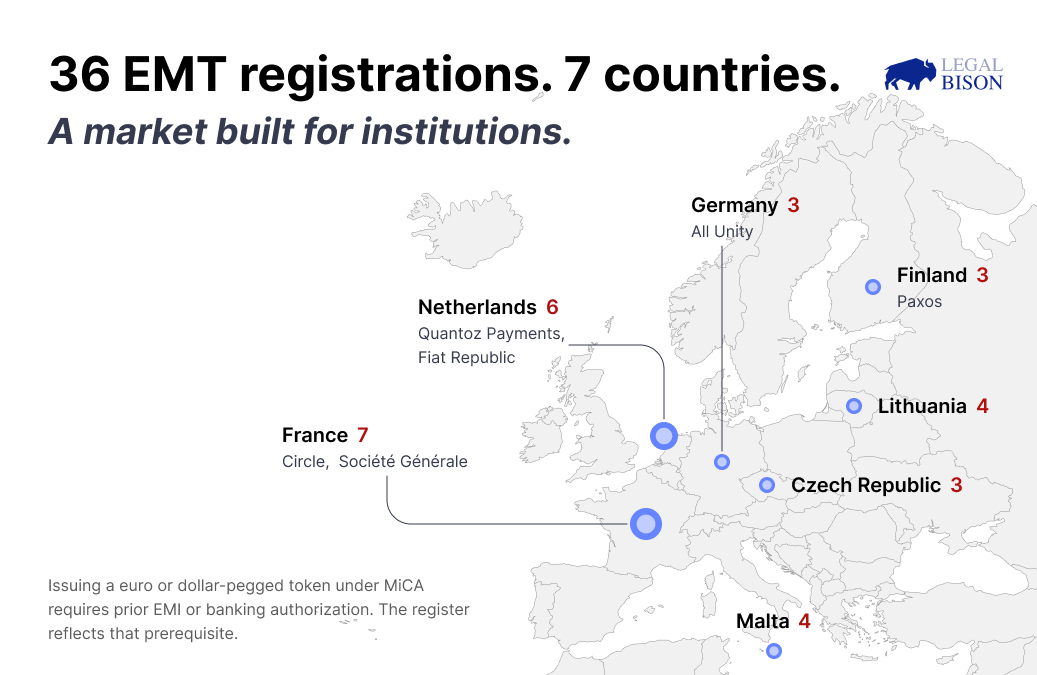

Ah, stablecoins, the darlings of the crypto world, pegged to fiat currencies, yet regulated under MiCA as Electronic Money Tokens (EMTs) or Asset-Referenced Tokens (ARTs). The EMT register contains 36 records, a number not low by accident. For issuing an EMT under MiCA requires prior authorization as an Electronic Money Institution (EMI) or a credit institution. A local entity is mandatory, and high capital and solvency requirements filter out startups at the entry point. The entities in the register? Banks and licensed payment institutions, not token-native projects.

France leads with 7 registrations, including Circle and Societe Generale, while the Netherlands holds 6, covering Quantoz Payments and Fiat Republic. Lithuania, Malta, Czech Republic, Finland, and Germany each hold 3 to 4 registrations. The remaining 6 are spread across other member states. France’s position at the top is not incidental, for the Autorité de Contrôle Prudentiel et de Résolution (ACPR) has a long track record supervising electronic money institutions, and Circle’s choice of France as its EU base anchors the most liquid dollar-denominated stablecoin in that jurisdiction.

For founders, the EMT market under MiCA is an institutional product category, defined by Circle, Societe Generale, and Paxos, not by early-stage teams. The path to EMT issuance begins with securing an EMI license or a banking authorization, a major hurdle that few can overcome.

What zero ARTs means

And what of ARTs, those tokens whose value references a basket of assets? The MiCA registers contain 761 other-crypto-asset white papers and 36 EMT white papers. The ART row reads zero. A category created for digital assets like DAI, yet the market gravitated towards single-asset backed stablecoins. The regulator’s intention was to address projects like Libra/Diem, a category that largely disappeared. The zero is not an anomaly, but a reflection of market preference, regulatory complexity, and capital cost.

Takeaways for projects seeking the right crypto license in Europe

- MiCA compliance for token issuance is operationally accessible to offshore entities. A BVI or Cayman company can satisfy the EU white paper requirement without moving its legal seat to Europe. The registration data confirms this common standard practice.

- Jurisdiction choice under MiCA still matters, as the approval process is heavily influenced by the regulator’s expertise and the underlying common law or civil law assumptions that shape their approach to white paper review.

- Ireland has processed the widest variety of token categories. Malta has the deepest local crypto compliance infrastructure. The Netherlands, Germany, and Luxembourg handle smaller volumes with different regulator profiles.

- While the proxy model facilitates market access for assets with no centralized issuer, it remains an impractical route for early-stage projects. Current industry standards, set by Kraken and LCX, prioritize the filing of white papers for high-volume tokens that already possess significant market depth.

- A token issuer seeking EU market access needs to engage the white paper process directly. For most projects, that means Ireland or Malta as the first practical option, regardless of where the legal entity is located.

- While the deadline for token issuers was in December 2024, the July 1, 2026, deadline for crypto-asset services applies to CASPs. But exchanges listing tokens for EU customers require a compliant white paper for each one. The closer that deadline gets, the less runway exists for token projects that have not yet filed. And the register data shows that the projects moving now are predominantly offshore.

LegalBison advises crypto and FinTech companies on MiCA licensing, CASP and VASP applications, token white paper compliance, and regulatory structuring across Europe and beyond. More information at legalbison.com.

This article is based on a study conducted by LegalBison in February 2026, with data updated as of March 12th, 2026. The content is for informational purposes only and does not constitute legal advice.

Read More

- XRP’s Price Tango: Can It Outdance the 100 EMA?

- Top 5 Hilarious Mistakes That Cost This Trader $2 Million on Polymarket! 😱💸

- Base Loses $1.4B: A Tragicomic Tale of Chains, Cash, and Clashing Visions

- 10M Crypto Users Targeted by Malware Ads!

- Silver Rate Forecast

- Gold Rate Forecast

- Bitcoin’s Plunge: A Tale of Woe and 0.3% Despair

- Ripple moves 250M XRP – Can supply crunch trigger a $2.50 move?

- 🚀 Solana’s $1B Treasury: A Celestial Heist or Cosmic Blunder? 🌌

- Bitcoin Mining Difficulty Plummets: The Universe’s Most Dramatic Haircut (Again)

2026-03-19 22:57