Markets, those pitiful mirrors of our souls, trembled on April 7 as Trump’s ominous warning-“a whole civilization will die tonight”-stood at the doorstep of the Hormuz deadline, and fear rushed into equities with the pomp of a carnival barker announcing doom.

WTI crude surged to $115.19, up 13% in a single week, a number that gnaws at the brain like a fever; reports of Israeli strikes on Iran’s Kharg Island petrochemical bastion erased the remaining de-escalation hopes that had briefly lifted the spirits of the market in recent sessions.

🚨 BREAKING: Trump warns ‘whole civilization will die tonight, never to be brought back again’ if Iran doesn’t agree to deal to end war

– Fox News (@FoxNews) April 7, 2026

Three forces dragged selling from the shadows on April 7, all tied to one root: oil above 115 stirs inflation fears, keeps the Fed shackled to its chair, and squeezes consumer and growth stocks as if one were squeezing the breath from a man in a dim room.

1. The Civilization Warning Kills De-Escalation Narrative

Markets had dallied with a faint de-escalation, a ghost of commerce whispered through mediators. Trump’s statement, issued before his self-imposed Tuesday deadline for Iran to reopen the Strait of Hormuz, shattered that specter and revived the dread of direct strikes upon Iranian energy infrastructure.

The Hormuz closure has already disrupted roughly one-fifth of global oil and LNG supplies. Trump’s demand for immediate reopening, paired with reports of Kharg Island strikes, signals that the conflict has entered a more dangerous chapter rather than winding down.

The Strait of Hormuz closure has disrupted a fifth of the world’s oil supply – and prospects for opening the strait soon look limited, at best.

What can we learn from this crisis? @aarondmiller2 hosts @CroftHelima to discuss.

April 7, 10am EDT, live online. RSVP:…

– Carnegie Endowment (@CarnegieEndow) April 2, 2026

Risk assets sold off as the “war ending soon” trade unwound, leaving the room to wonder if we were all spectators to a tragedy with an audience of one-the man with the microphone.

2. WTI at $115 Tightens the Oil-Inflation-Rates Chain

WTI crude at $115.19 sits like a blunt instrument, 13% higher in a single week. Oil at these levels acts as a direct tax on consumers and businesses, lifting input costs across every sector and feeding into the inflation data the Federal Reserve is watching with that stern, almost religious gaze.

The March CPI report due Friday is expected to show the sharpest monthly increase since 2022, making rate relief seem a distant memory and perhaps a cruel joke played on patience.

Inflation Shock Meets Policy Paralysis

March US CPI is expected to jump 1%, the sharpest monthly rise since 2022, after the Iran war added roughly $1 a gallon to petrol prices, while core CPI is still seen rising 0.3% and core PCE likely prints 0.4% for a third straight month.…

– Bancara (@Bancaraglobal) April 6, 2026

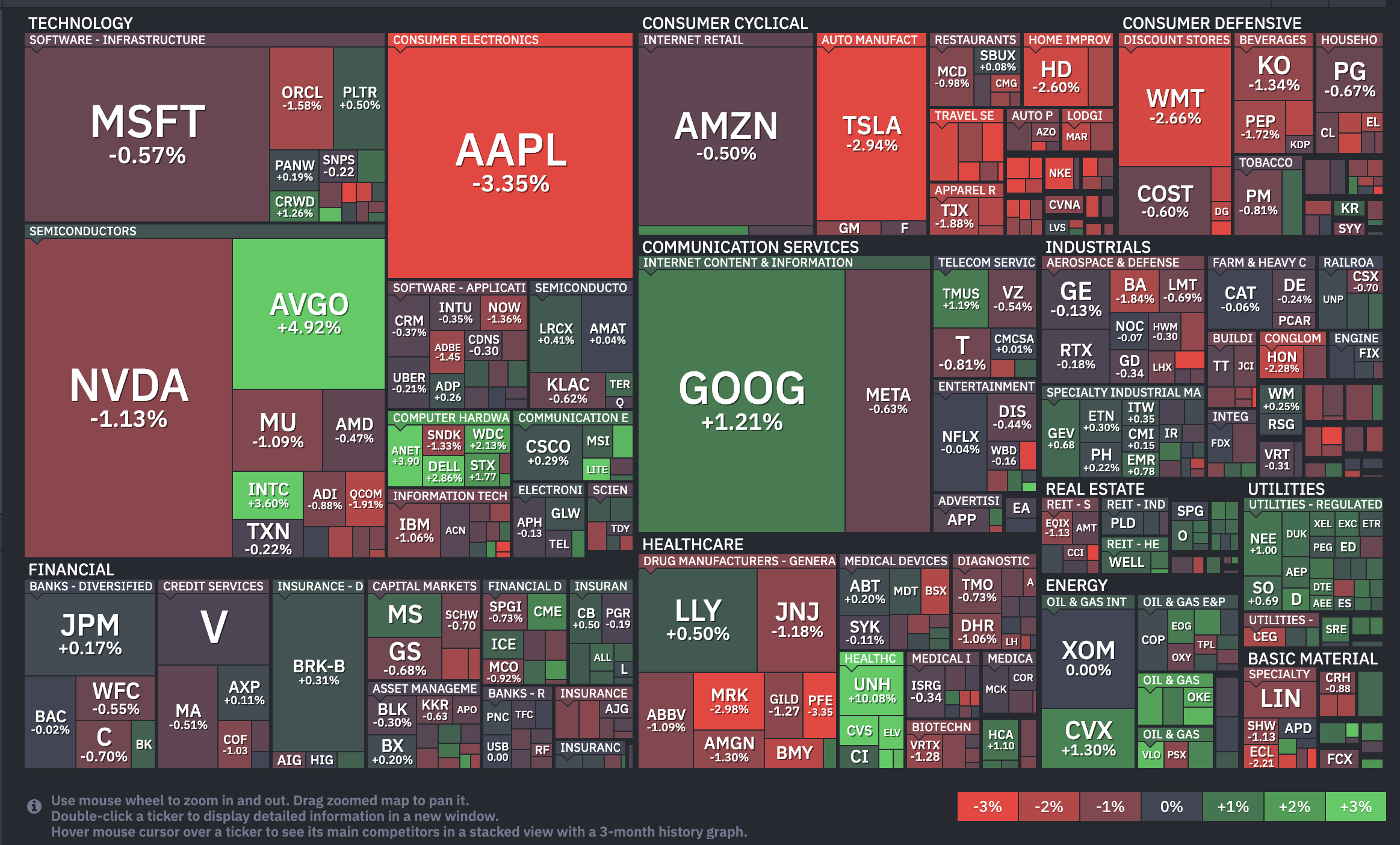

3. Apple’s 3.35% Drop Drags the Index

Apple (AAPL) fell 3.35% after Nikkei Asia reported engineering setbacks in the foldable iPhone that could push back production timelines. Apple carries the largest weighting in the S&P 500, so a nearly 4% decline mechanically drags the index regardless of broader conditions.

Apple shares sink 4% on report of foldable iPhone delays

– CNBC (@CNBC) April 7, 2026

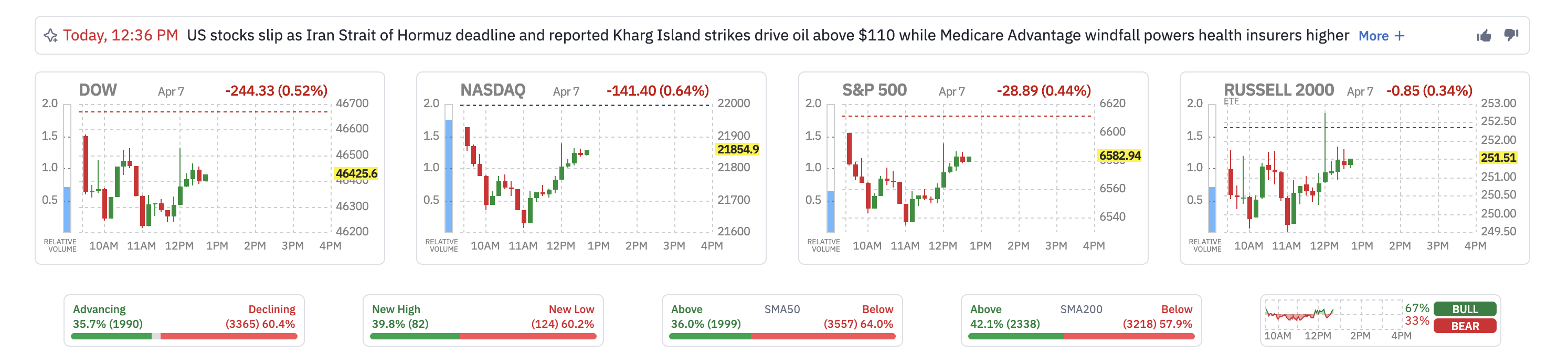

What Is Happening to Major US Indexes?

At press time, all four major indexes are in the red, as if the city itself were bowing its head in a confession.

- S&P 500 fell 28.89 points (−0.44%) to 6,582.94. The index dipped over 1% earlier in the session before recovering.

- Dow Jones Industrial Average dropped 244.33 points (−0.52%) to 46,425.60.

- Nasdaq Composite declined 141.40 points (−0.64%) to 21,854.90.

Russell 2000 slipped 0.85 points (−0.34%) to 251.51, a quiet echo that small caps echo the broader sorrow.

Market breadth is negative, with 3,365 stocks declining (60.4%) versus 1,990 advancing (35.7%).

The S&P 500 trades at 6,580 on the daily chart, grappling with two converging Exponential Moving Averages, those sly guardians of price action that pretend to know what the market will do next.

The 20-day EMA sits at 6,601 and the 200-day EMA at 6,587. When the shortest and longest EMAs compress this tightly, one feels the market has lost direction and waits for a catalyst-perhaps a prayer, perhaps a shove from fate.

The intraday low of 6,534 found support near 6,518 at the 0.382 technical level. A daily close below 6,518 opens the path toward 6,441 and the previous swing low at 6,316.

On the upside, the US stock market needs a daily close above 6,643 to show recovery strength, with 6,845 as the next target beyond that-an almost sacred number, if such a thing exists in charts.

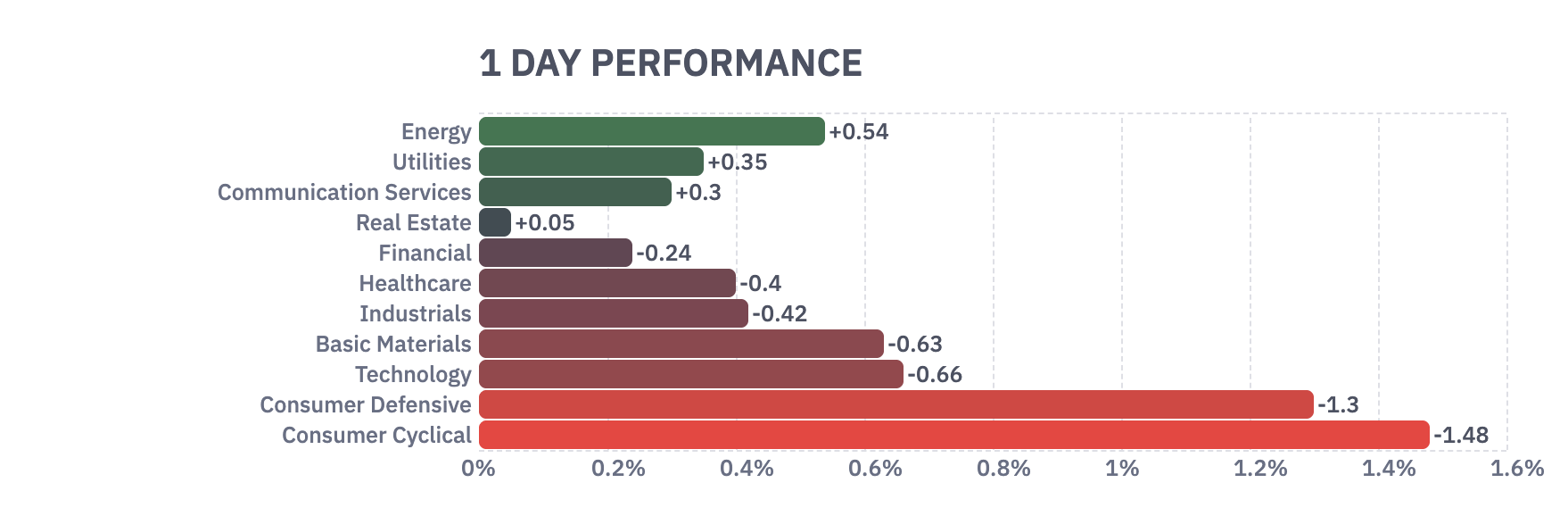

Which Sectors Are Holding Up?

Energy led with a +0.54% gain as WTI stayed above $115. The sector remains the only group with a structural tailwind from the Iran conflict, as elevated oil prices directly increase producer revenue.

Utilities added +0.35% as defensive positioning continued. Risk aversion is overriding the sector’s traditional rate sensitivity, making yield-paying defensives attractive as a parking spot for nervous capital.

Communication Services gained +0.30%, supported by Google (GOOG) rising 1.21%.

Which Sectors Are Falling?

Consumer Cyclical led losses at −1.48%. Higher oil prices compress discretionary spending power by raising fuel and transportation costs. Tesla (TSLA) fell 2.94%, Home Depot (HD) dropped 2.60%, and Walmart (WMT) lost 2.66%.

Consumer Defensive also fell 1.30%, an unusual decline for a traditionally safe sector that signals selling pressure is broad enough to touch even conservative holdings. Coca-Cola (KO) lost 1.34% and Procter & Gamble (PG) dropped 0.67%.

Basic Materials declined 0.63% despite gold holding above $4,400. The slide reminds us that commodity-linked equities are not fully insulated from the storm outside.

Major Stock News Investors Are Watching

Broadcom (AVGO) jumped 4.92% after Anthropic signed an agreement with Google and Broadcom for multiple gigawatts of next-generation TPU capacity starting in 2027.

The deal signals that AI infrastructure demand remains strong enough to override the macro headwinds for companies directly tied to capacity buildout.

We’ve signed an agreement with Google and Broadcom for multiple gigawatts of next-generation TPU capacity, coming online starting in 2027, to train and serve frontier Claude models.

– Anthropic (@AnthropicAI) April 6, 2026

UnitedHealth Group (UNH) surged 10.08% on Medicare Advantage windfall news, making it the day’s standout gainer in the S&P 500 and providing a floor for the Healthcare sector that would have otherwise fallen further.

What Are Investors Watching Next?

Trump’s self-imposed Tuesday deadline for Iran to reopen the Strait of Hormuz arrives within hours. If Iran signals compliance or a negotiated pathway, oil could retreat sharply, lifting equities by Wednesday’s open.

If the deadline passes without resolution and strikes on Iranian energy infrastructure begin, WTI could push higher. That scenario would further compress the oil-inflation-rates chain. It would push the 10-year yield toward new highs, and bring the S&P 500’s 6,316 swing low firmly into play.

The March CPI data arrives on Friday. A hot print would reinforce the “higher for longer” narrative, while a softer number could provide relief to growth stocks.

The combination of the Iran deadline and CPI makes this week one of the most event-dense mornings in the life of the US stock market.

Read More

- Brent Oil Forecast

- USD VND PREDICTION

- HYPE PREDICTION. HYPE cryptocurrency

- DOGE PREDICTION. DOGE cryptocurrency

- Silver Rate Forecast

- CNY RUB PREDICTION

- CNY JPY PREDICTION

- ONDO PREDICTION. ONDO cryptocurrency

- FIL PREDICTION. FIL cryptocurrency

- USD CNY PREDICTION

2026-04-07 20:56