What to know:

Welcome to Crypto Long & Short, the newsletter that’s more confusing than a blockchain fork at a family reunion! Sign up here to get it in your inbox every Wednesday, whether you like it or not!

This week, we’re diving into the wild world of crypto governance, where the only thing more unstable than the price of Bitcoin is the decision-making process. Buckle up!

- Nilmini Rubin explains why crypto and TradFi are like a bad marriage-they need a hybrid governance structure, but neither wants to do the dishes.

- Meredith Fitzpatrick reveals why financial institutions are rethinking AML risk faster than a rug pull in a DeFi project.

- Francisco Rodrigues brings you the headlines that will make you question if crypto is a revolution or just a really expensive joke.

- Maple loans hit $1 billion, proving that even in crypto, someone’s still lending money to people who can’t pay it back.

-Alexandra Levis, your friendly neighborhood crypto translator.

Expert Insights

Governance is the real Layer 1 (or is it Layer Chaos?)

By Nilmini Rubin, chief policy officer, Hedera (aka the person trying to make sense of this mess)

Remember when Silicon Valley Bank collapsed in 2023? USDC lost its dollar peg faster than a politician loses their promises. Billions were trapped, markets stalled, and everyone panicked like it was the end of the world. Spoiler alert: it wasn’t. But it did expose a new risk-traditional finance can directly impact digital assets. Who knew?

Now, imagine if the risk went the other way. Who intervenes? Who absorbs the losses? And how do we restore confidence in markets? Spoiler alert #2: No one knows. But hey, at least we’re innovating, right?

As blockchains start underpinning financial markets, the next phase of digital assets will be defined by coordinated accountability. Or, as I like to call it, “figuring out who’s in charge before everything blows up.”

The false binary (or, why can’t we all just get along?)

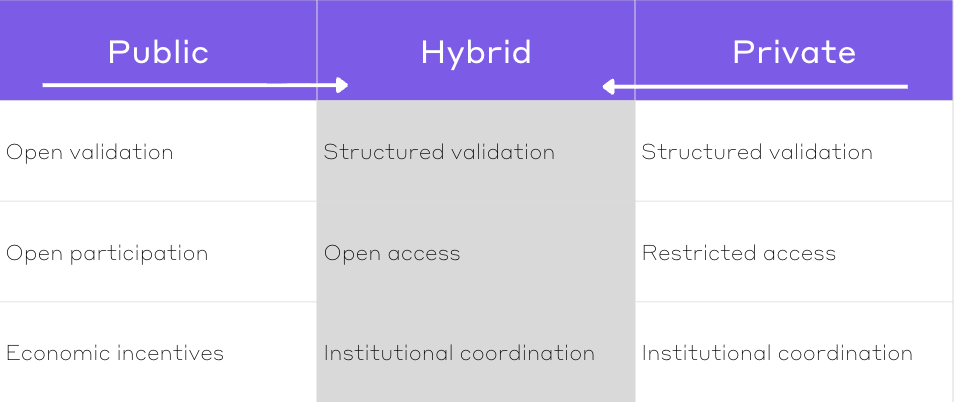

For years, blockchain debates have been like a bad reality show: public vs. private networks. Permissionless networks are like the wild child-open and rebellious but can’t handle upgrades or emergencies. Private systems are the control freak-compliant but not very fun. Hybrid models are the compromise child, trying to please everyone and failing spectacularly.

Blockchain architecture: because why have one problem when you can have two?

When governance meets crisis (or, the blind leading the blind)

In complex systems, responsibilities are usually defined before problems emerge. Unless you’re in crypto, where we prefer to figure it out as we go. When stress arrives-sanctions, protocol failures, market crashes-governance becomes the ultimate test. Spoiler alert #3: We’re failing.

Remember the March 2020 market crash? MakerDAO needed emergency intervention after auction failures erased millions. They recovered, but let’s not make a habit of this, okay? And don’t get me started on coordinated forks-they’re like putting a band-aid on a bullet wound.

As tokenization expands, resilience will require governance systems that anticipate crises. Or, you know, just hope for the best.

Putting governance to the test (or, how to fail gracefully)

Mature financial systems stress-test their governance structures. Hybrid networks need to do the same. Governance stress testing clarifies roles, aligns incentives, and strengthens coordination. It’s like a fire drill, but for your blockchain. Let’s hope no one panics.

Governance is the real Layer 1 (or, the only thing more important than code is who’s writing it)

Digital assets are reimagining ownership and participation. The next challenge? Figuring out who’s in charge. The networks that endure won’t be the ones with the most tokens or the fastest throughput. They’ll be the ones that don’t collapse under pressure. Good luck!

Headlines of the Week (or, the crypto circus never stops)

– By Francisco Rodrigues, your ringmaster of chaos

The crypto industry is navigating the regulatory system like a drunk sailor-stumbling into the mortgage market while being stopped from offering yields on stablecoin balances. Trust is building, even as prices drop. It’s like a bad magic show: now you see it, now you don’t.

- Stablecoin yield in crypto Clarity Act won’t allow rewards on balances. Because why let people make money when you can just ban it?

- UK political crypto donations banned. Because nothing says “trust” like banning transparency.

- Coinbase and Fannie Mae bring crypto-backed mortgages. Because why not gamble on both housing and crypto at the same time?

- Tether hires a ‘Big Four’ firm for a full audit. Finally, someone’s checking if the emperor has clothes.

- Nearly half of all circulating bitcoin is underwater. Long-term holders are selling at a loss. Surprise, surprise.

Expert Perspectives

The new financial order: updating TradFi risk for crypto (or, how to not get rug-pulled)

– By Meredith Fitzpatrick, partner and head of cryptocurrency, Forensic Risk Alliance (aka the person who cleans up the mess)

Traditional finance and cryptocurrency are converging faster than a meme coin pump and dump. Regulatory clarity is accelerating institutional entry, but many institutions are treating crypto like it’s just another product. Spoiler alert #4: It’s not. Crypto fundamentally changes how AML risk must be assessed, monitored, and controlled. It’s like trying to herd cats, but the cats have private keys.

Control shifts from accounts to keys (or, the wild west of cybersecurity)

In TradFi, assets are secured through centralized systems. In crypto, control rests with private keys. When institutions offer custody, AML risk becomes inseparable from cybersecurity risk. A compromised key isn’t just a breach-it’s an irreversible transfer of value. Multi-signature authorization, cold storage, strict access governance, and wallet segregation are now critical. Good luck fitting that into your existing AML framework.

Non-custodial wallets mean dynamic risk assessments (or, the identity crisis)

Traditional AML relies on customer identity and static risk profiling. In crypto, this model breaks down faster than a poorly written smart contract. Customers can transact through non-custodial wallets, and illicit activity often hides in transaction behavior. Risk assessment must evolve from “who the customer is” to “what the wallet does.” Continuous monitoring of on-chain activity is now a must. Welcome to the future.

Crypto financial crime is structurally more complex (or, the game of blockchain whack-a-mole)

Cryptocurrency money laundering involves chain-hopping, mixers, and privacy-enhancing technologies. Transactions can traverse multiple jurisdictions in minutes, rendering legacy screening systems useless. Effective AML now depends on blockchain intelligence. Trace funds, identify exposure to risky parties, and interpret transaction patterns. It’s like detective work, but with more math.

Area of focus |

TradFi |

Crypto |

|---|---|---|

| Customer identity | Government IDs, physical addresses, and credit history. Because who doesn’t love paperwork? | KYC/CDD/EDD for centralized VASPs, but non-custodial wallets exist outside KYC. On-chain activity is your new best friend. |

| Risk indicators | Employment, income, geography, and transaction history. Boring, but effective. | Wallet behavior, transaction counterparties, interactions with high-risk services, and exposure to DeFi platforms. Exciting, but complicated. |

| Transaction transparency | Private and accessed through internal records. Because secrets are fun. | Publicly available on-chain transactions. Advanced analytics required. Good luck! |

| Dynamic risk monitoring | Static or periodically updated. Because change is scary. | Dynamic with real-time blockchain analysis. Because crypto never sleeps. |

Institutions must invest in new capabilities. Blockchain analytics for transaction monitoring and forensic investigation are now core AML functions. Most will need a hybrid model combining internal expertise with external specialists. Crypto compliance isn’t just adapting existing frameworks-it’s a fundamental transformation. Good luck, and may the odds be ever in your favor.

Chart of the Week

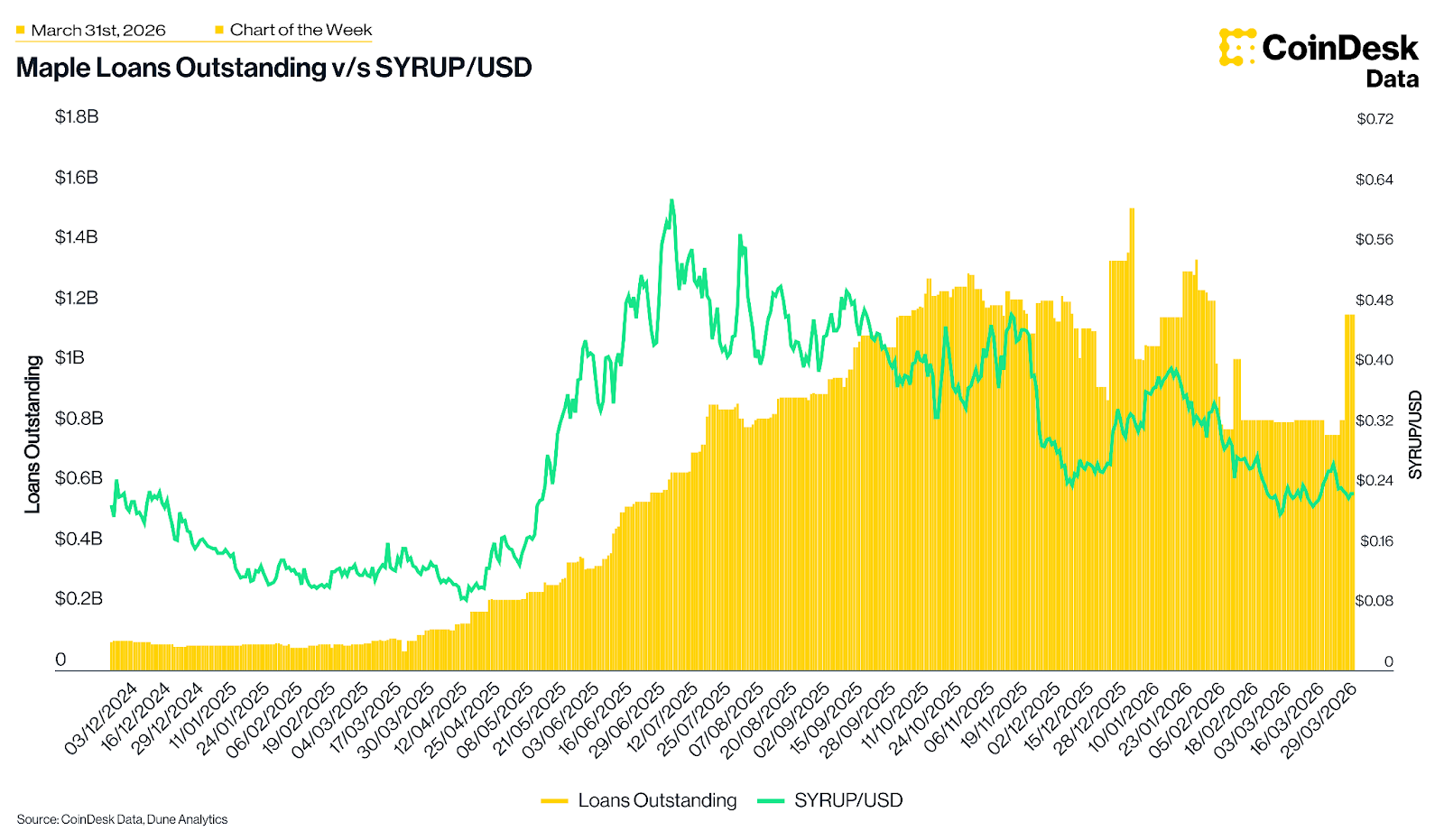

Maple loans surge past $1B on record $350M single-day issuance (or, when it rains, it pours)

Maple’s loans outstanding jumped back above $1 billion last week, with $350 million issued in a single day. Total AuM now exceeds $4.6 billion, but the SYRUP token price action tells a different story. Growth continues despite broader market conditions, highlighting resilient demand for institutional-grade lending. Or, as I like to call it, “lending money to people who can’t pay it back, but with blockchain.”

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions. Because who doesn’t love more chaos?

Read More

- Nevada Slaps Kalshi with 14-Day TRO-Prediction Markets in Jeopardy!

- UK Cracks Down on Crypto Exchange with a Side of Fake IDs and Big Military Money

- Brent Oil Forecast

- 🤑 Crypto ATM Scams: Will Senators Save Grandma’s Fortune? 🕵️♂️

- Crypto King Buys £22M Mansion While UK Market Cries “Poor Me”

- Gemini’s Wallet: Web3 Meets Passkeys Without the Crypto Cringe 😂

- Uniswap Outwits Fraudulent Fools in Legal Farce!

- FTX’s Fourth Payout: A $2B Windfall or a Desperate Gamble?

- EUR INR PREDICTION

- Silver Rate Forecast

2026-04-01 20:01