Ah, the world of decentralized finance, where the only thing more volatile than the token prices is the jargon. One day you’re a “liquidity miner,” the next you’re a “yield aggregator,” and before you know it, you’re a “Risk Curator” sipping artisanal coffee while pondering the intricacies of “RWA-backed lending.” It’s enough to make your head spin faster than a Solana validator.

TL; DR

- Lending is evolving from a “direct-to-protocol model for everyone” toward a structure of “protocol infrastructure + strategy layer.” Curators package institutional-grade risk management, portfolio construction, and routing into non-custodial vaults, with their share steadily increasing. Meanwhile, the growing complexity of RWA is making verifiable risk frameworks such as PoR and DVN increasingly essential. (Think of it as DeFi’s version of hiring a personal trainer for your portfolio.)

- RWA are no longer merely held on-chain; they are evolving into yield-bearing, collateralizable, and composable building blocks for on-chain strategies. Platforms and Curators are driving the growth of multi-asset RWA vaults and related derivatives, while institutions are increasingly integrating with DeFi through infrastructure-level partnerships. (Basically, your grandma’s Treasury bonds are now getting a blockchain makeover.)

- CEXs and wallets focus on user acquisition, user experience, and compliance, while DeFi handles yield execution, settlement, and risk management. In practice, users access “one-click” lending and yield products on CEX platforms, with the underlying strategies driven by on-chain protocols and Curator-managed vaults. (It’s like ordering a fancy coffee from a hipster barista, but the beans are roasted on a blockchain.)

- As the yield layer scales, projects are expanding into payments, accounts, and cards-forming a closed loop from “save → grow → spend.” Whether this model can scale will depend on whether regulation can establish baseline safeguards and clear accountability, while preserving the advantages of on-chain verifiability. (Will DeFi finally grow up and get a real job, or will it remain the rebellious teenager of finance?)

Introduction

Remember the good old days of DeFi, when “liquidity mining” sounded like something you’d do in a video game and “yield aggregators” were the new hotness? Well, buckle up, buttercup, because the DeFi landscape has evolved faster than a meme coin pump and dump. From the early days of “APY farming” to the current craze for “looped lending” and “Pendle points farming,” the surface mechanics of yield generation may seem like a never-ending game of financial Whac-A-Mole. But beneath the hype, the core principle remains: risk and reward are still dancing the same old tango.

Take cash and Treasury bills, the financial equivalent of a warm blanket and a cup of chamomile tea. These assets are as “risk-free” as a catnap in a sunbeam, typically represented by short-term U.S. Treasuries and money market funds. Historically, they’ve delivered returns around 3.3%, but after inflation takes its cut, you’re left with the financial equivalent of a participation trophy.

Bonds, on the other hand, are like a rollercoaster ride through the financial theme park. Whether issued by governments or corporations, they offer higher returns but come with a healthy dose of “credit risk,” “duration volatility,” and “liquidity risk.” It’s like betting on a horse race: you might win big, but you could also end up holding a losing ticket.

And DeFi? Well, it’s like the Wild West of finance, where the returns can be stratospheric, but the risks are often hidden behind a curtain of complex smart contracts and obscure tokenomics.

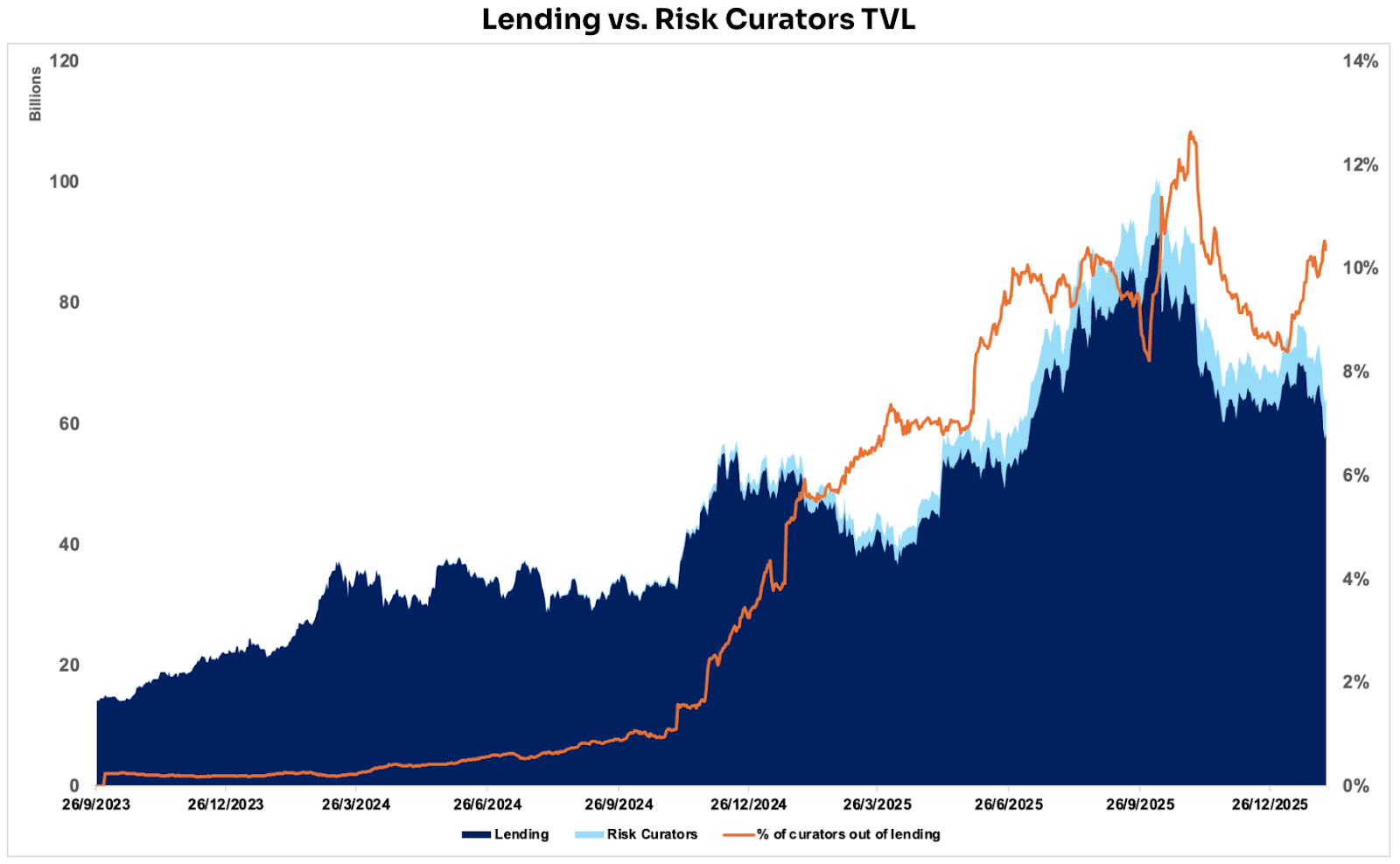

Trend 1: Lending Markets Become Modular, Driven by Risk Curators

Remember when everyone was a “degen” yield farmer, throwing their crypto into any protocol promising double-digit APYs? Those days are as gone as a fidget spinner fad. The on-chain lending market has matured, and it’s now a sophisticated ecosystem where “Risk Curators” are the new sheriffs in town. These are the folks who package institutional-grade risk management, portfolio construction, and routing into non-custodial vaults, essentially acting as DeFi’s version of hedge fund managers.

Think of it like this: DeFi 1.0 was a financial free-for-all, where everyone had equal access to the same protocols and information. But as the stakes got higher, the need for professional risk management became apparent. Enter the Risk Curators, who are essentially the financial architects of DeFi 2.0, building complex strategies and making them accessible to the masses.

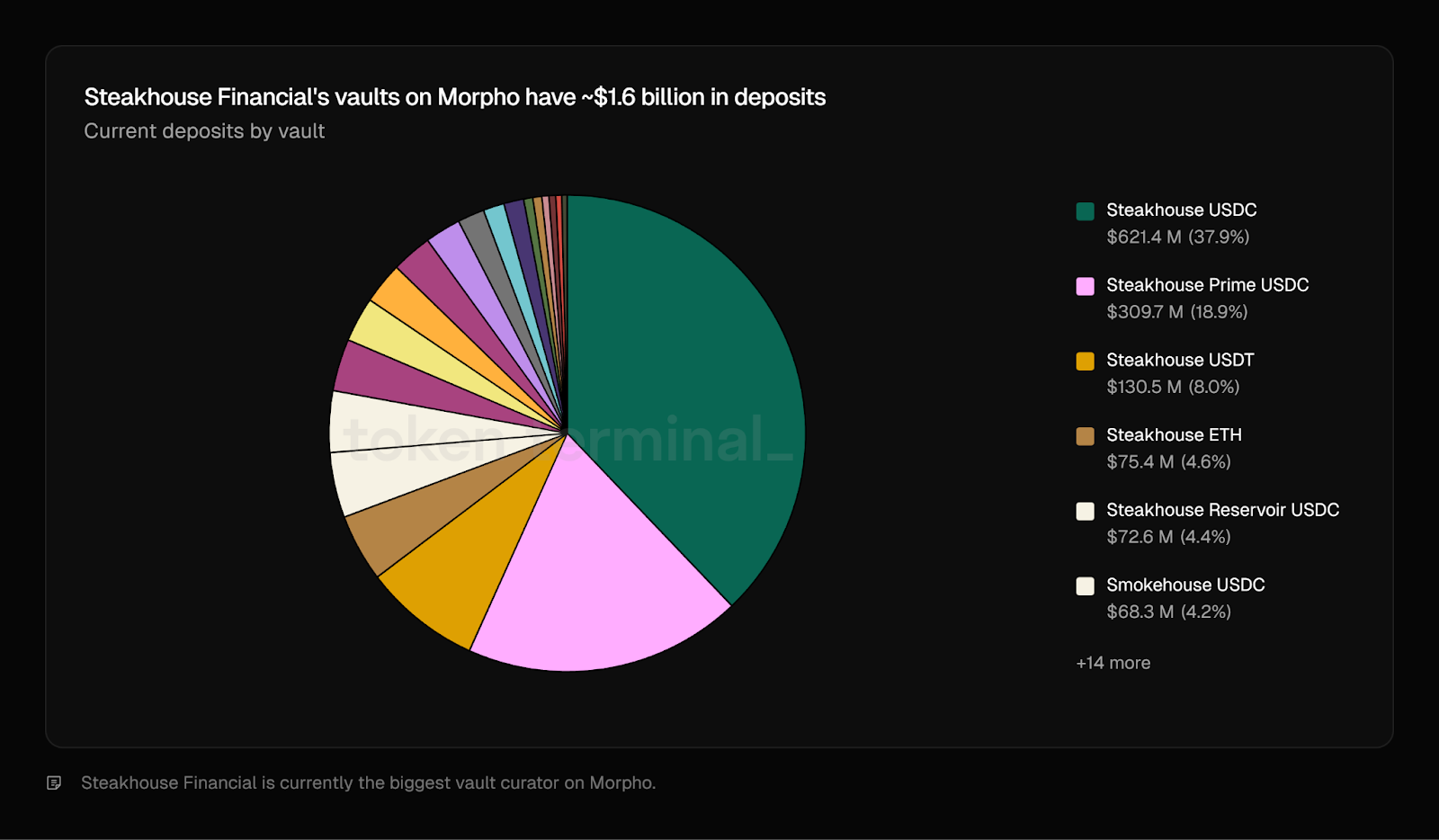

And these Curators are no small fish. Steakhouse Financial, Sentora, and Gauntlet are managing billions in on-chain lending positions, proving that DeFi is no longer just a playground for crypto cowboys.

How did these on-chain asset managers become the new DeFi titans?

It’s not just about who’s got the biggest wallet. As DeFi infrastructure matures and specialization deepens, both the supply and demand sides of the market are flourishing. Think of it as a symbiotic relationship: protocols like Morpho provide the rails, while Curators like Steakhouse build the fancy trains that run on them.

(1) Product Layer: Curators package their risk management expertise into accessible “non-custodial funds,” allowing users to achieve better risk-adjusted returns without having to become crypto trading wizards.

(2) Risk Management Layer: They replace “trust” with verifiable mechanisms like timelocks and delayed changes, ensuring that your funds aren’t at the mercy of a single rogue actor.

(3) Distribution Layer: Curators are expanding beyond the crypto-native crowd, partnering with platforms like Coinbase to bring DeFi yields to a wider audience.

Why is this becoming a trend?

Because DeFi is growing up. As RWA (real-world assets) enter the fray, the complexity of risk management skyrockets. Curators are the ones who can navigate this new landscape, screening and structuring complex risks, and making RWA-backed lending accessible to everyday users.

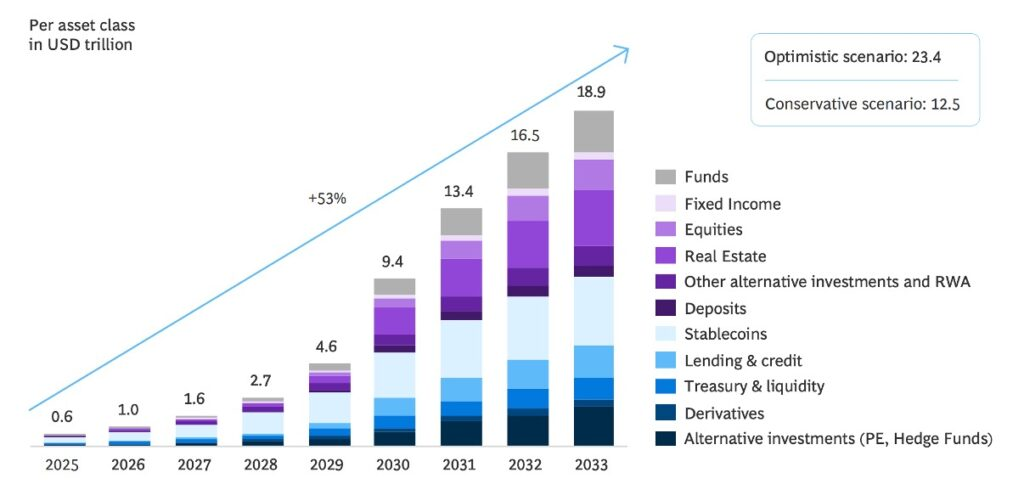

Trend 2: RWA Matures On-Chain as DeFi Use Cases Continue to Expand

Remember when “tokenizing” assets meant slapping a blockchain sticker on a JPEG? Well, RWA is taking tokenization to a whole new level. We’re talking about bringing trillions of dollars worth of real-world assets, from Treasury bills to reinsurance premiums, onto the blockchain. It’s like giving your grandma’s jewelry box a digital upgrade.

But it’s not just about slapping a blockchain label on things. RWA are becoming yield-bearing, collateralizable, and composable building blocks for on-chain strategies. Think of them as Lego bricks for DeFi, allowing builders to create complex financial structures with real-world assets as the foundation.

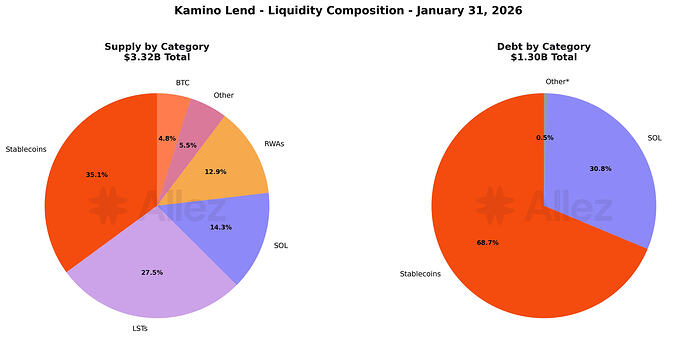

Lending Platforms

Platforms like Aave, Morpho, and Kamino are leading the charge, integrating RWA into their core offerings. Aave’s Horizon is turning RWA lending into a compliant, standalone modular market, while Morpho is using Curator Vaults to make RWA-backed lending accessible to a wider audience. Kamino, meanwhile, is attracting Risk Curators to build and execute a variety of RWA yield strategies on its platform.

The result? A shift in collateral composition, with stablecoins and RWAs now dominating the lending landscape. It’s a clear sign that DeFi is moving beyond its crypto-native roots and embracing the real world.

Growing Institutional Adoption of DeFi

Even the stodgy world of traditional finance is starting to take notice. Institutions are no longer just dipping their toes into DeFi; they’re diving in headfirst, integrating compliant RWAs directly into DeFi’s trading and liquidity rails. Think of it as Wall Street finally acknowledging that blockchain isn’t just a fad.

The Uniswap x BlackRock collaboration is a prime example. By connecting BlackRock’s tokenized money market fund to UniswapX, they’re enabling qualified investors to trade and route liquidity between traditional assets and DeFi in a seamless way. It’s like building a bridge between the old financial world and the new.

RWA Perpetuals

And then there are RWA perpetuals, the financial equivalent of a rollercoaster with no brakes. These derivatives allow traders to gain exposure to real-world assets without actually owning them, opening up a whole new world of speculative possibilities. But beware, the ride can be bumpy, and the regulatory landscape is still a work in progress.

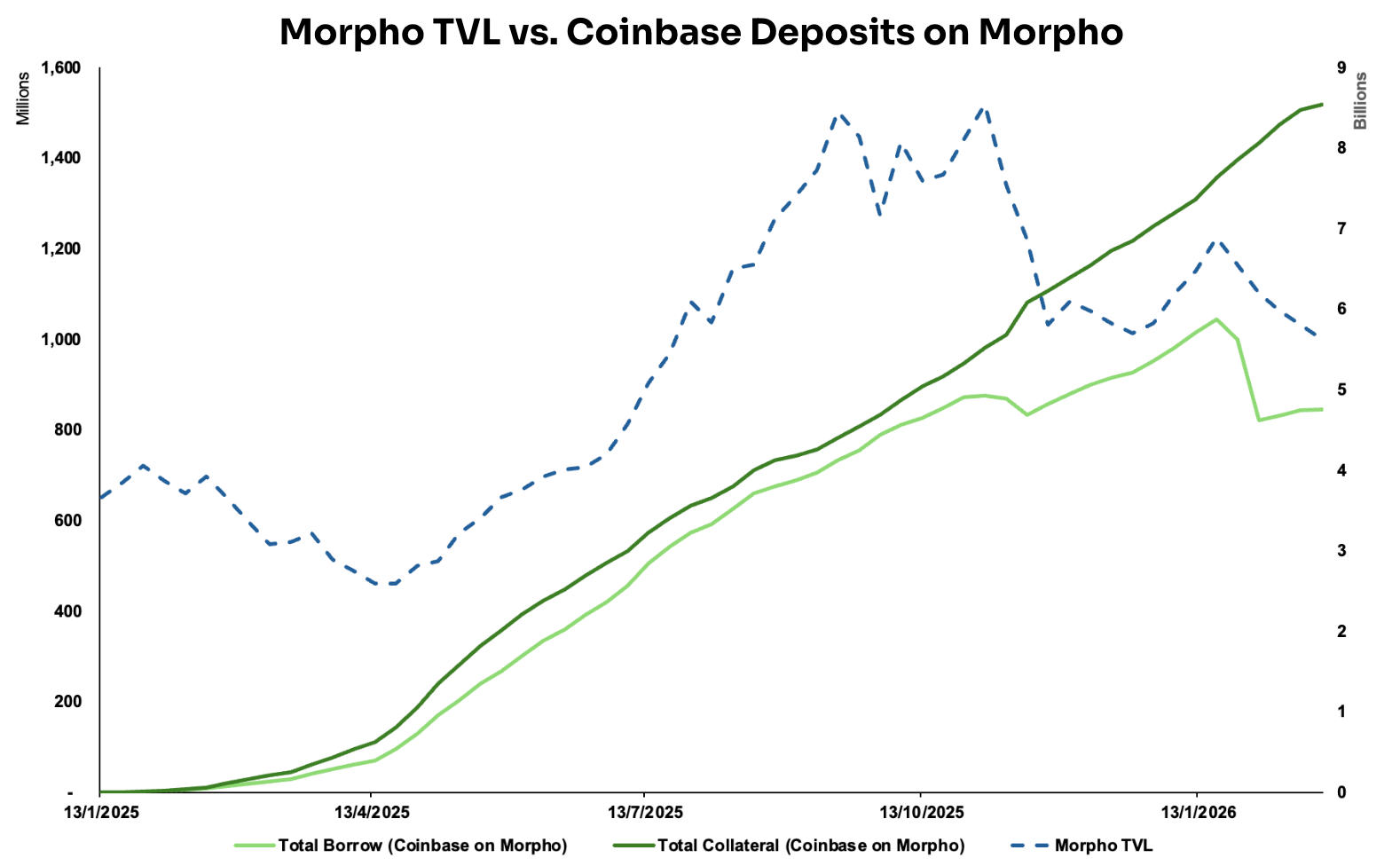

Trend 3: DeFi Becomes the Yield and Execution Infrastructure for Centralized Distribution

Remember when DeFi was all about “decentralization” and sticking it to the man? Well, it turns out that even the most die-hard crypto anarchists need a user-friendly interface. That’s where centralized exchanges (CEXs) come in. They’re becoming the front door to DeFi, providing users with a familiar and accessible way to access yield products, while DeFi protocols handle the heavy lifting in the background.

Think of it as a symbiotic relationship: CEXs handle user acquisition, productization, and compliance, while DeFi protocols focus on yield execution, settlement, and risk management. It’s a win-win situation, allowing DeFi to reach a wider audience while leveraging the strengths of centralized platforms.

The Coinbase and Morpho partnership is a perfect example. Coinbase users can now borrow USDC using Bitcoin as collateral, all while the complex on-chain interactions are handled seamlessly in the background. It’s DeFi made easy, thanks to the power of centralized distribution.

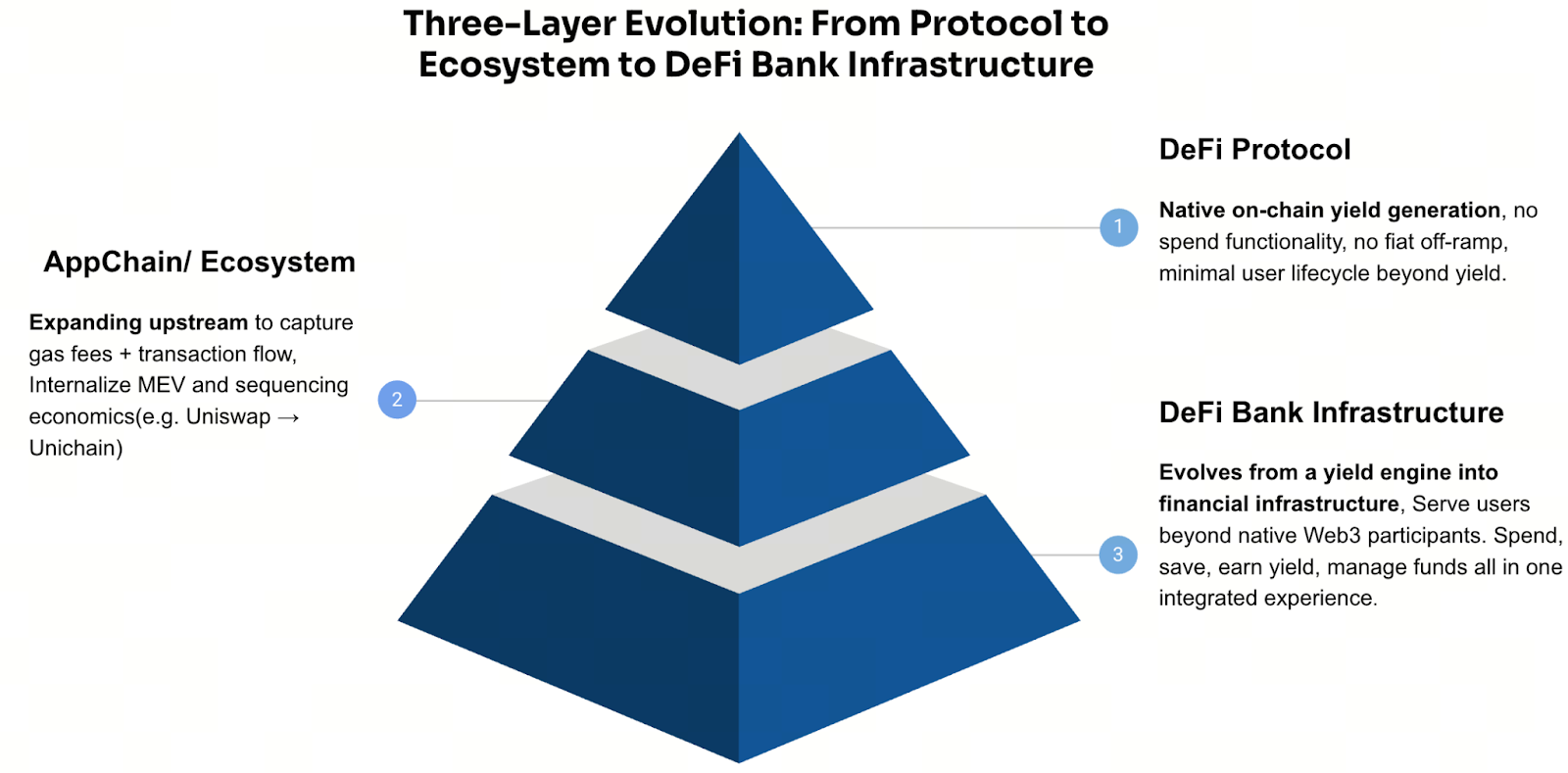

Trend 4: DeFi Vaults Upgrading into On-Chain Neo-Banks Integrating Payments, Savings, and Yield

The ultimate goal of DeFi? To become your one-stop shop for all things finance. Projects like ether.fi and Tether are leading the charge, evolving from single-purpose protocols into full-fledged financial ecosystems. They’re offering savings accounts, yield generation, payment services, and even debit cards, blurring the lines between traditional banking and the decentralized world.

But can DeFi truly replace traditional banks? That remains to be seen. While DeFi offers transparency and control, it lacks the safety nets of traditional finance, like deposit insurance and a lender of last resort. The success of DeFi banks will ultimately depend on regulatory clarity and the development of robust risk management mechanisms.

One thing is certain: the financial landscape is changing, and DeFi is playing a major role in shaping its future. Whether it’s through Risk Curators, RWA integration, or the rise of neo-banks, DeFi is no longer a niche experiment. It’s a force to be reckoned with, and its impact will be felt for years to come.

Read More

- Gold Rate Forecast

- Silver Rate Forecast

- ADA to $1.00? 🧐 A Most Curious Ascent!

- CRV PREDICTION. CRV cryptocurrency

- Shiba Inu’s SHIB Plummets: 70% Crash Alert!

- Dogecoin’s Dilemmas: Will the Canine Coin Fetch Its Fortune?

- Crypto Market: Cooling Demand and a Niche Party, Not a Full-Blown Alt-Season 🚨

- Trump’s Fed Fiasco: Judge Saves Cook from the Orange Flame🔥

- Sir Bitcoin’s Delicate Predicament: A Cautionary Dance of Bulls vs. Bears 🐘💔

- Ripple CEO: Banks Are Hoarding Profits While America Waits for Clarity!

2026-03-18 11:24