$IREN, in a feat of financial acrobatics worthy of a circus tent and a stiff gin, managed to secure 96% of its $5.81bn GPU capex for its Microsoft contract-at a financing cost so low it might as well have been found under a sofa cushion. The trick? Using the Microsoft lease as collateral, which conveniently carries an investment‑grade rating.

-

Key Takeaways:

- IREN secured $3.65B on Jun. 1; Microsoft’s looming presence scared financing costs down to 6.00%.

- Fitch rated IREN’s facility A; pension capital may now wander into AI infrastructure like tourists who took a wrong turn.

- CoreWeave’s $8.5B deal set the tone; TeraWulf and Cipher now sprint after similar sugar daddies.

If you’ve been following Bitcoin mining stocks for any length of time, you’ll know the usual ritual: companies need cash, companies issue shares, your ownership shrivels like a neglected houseplant. Dilution has been the industry’s favorite pastime.

Which is why IREN’s latest financing maneuver felt like spotting a unicorn in a parking lot. The company-now insisting it is an AI cloud provider rather than a Bitcoin miner with a side hustle-raised $3.65B in debt at an investment‑grade rating without issuing a single new share. I reread the terms twice, then checked for hidden cameras. The how is the real entertainment here.

What IREN actually did

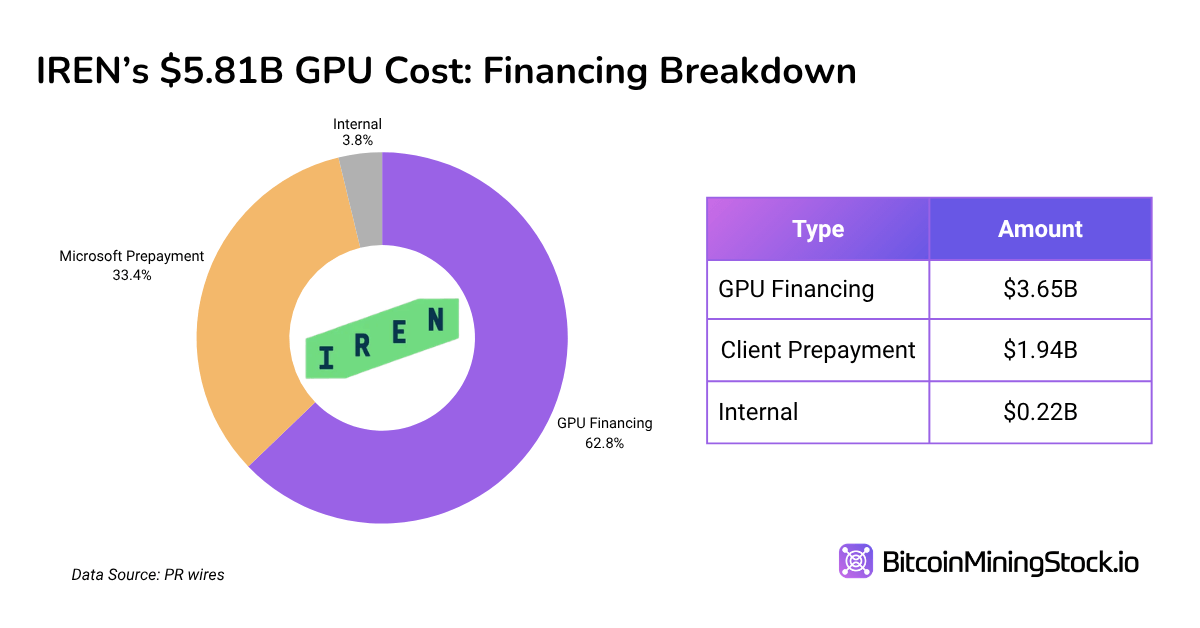

On June 1, IREN (NASDAQ: IREN) closed a $3.65B facility to buy GPUs for its AI cloud contract with Microsoft. The terms: a blended cost of 6.00%, arranged by Goldman Sachs and J.P. Morgan-two institutions that rarely get out of bed for anything less than a billion. The loan is secured against the GPUs and Microsoft’s contracted payments, which is rather like borrowing money using Buckingham Palace as collateral.

Then Microsoft, in a gesture of corporate benevolence (or self‑interest, depending on your cynicism levels), prepaid $1.94B of the bill. Between the loan and the prepayment, IREN covered about 96% of its $5.81B GPU cost without touching its own wallet. All this to serve a contract worth $9.7B over five years. Not bad for a company that once dug digital coins out of the metaphorical dirt.

Management claims it “essentially got the GPUs for next to nothing,” quoting an all‑in cost of 3.31%. Charming optimism. That number treats Microsoft’s prepayment as free money, when in reality it’s more like borrowing your neighbor’s lawnmower-you’ll return it eventually, and probably with a scratch. The real cost is 6.00%. Which leads to the question: how does a company in this sector borrow billions at 6% when the debt markets previously treated them like uninvited guests? The answer: credit rating magic.

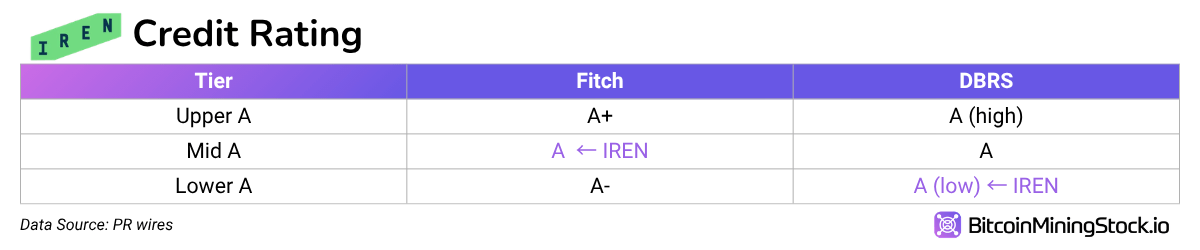

How the deal earned an investment‑grade rating

The facility was rated A by Fitch and A (low) by DBRS. A credit rating is essentially a polite way of saying how likely you are to pay your bills. Here’s how the “A” band stacks up:

Anything BBB or above is investment grade. Below that, you enter the realm of “speculative grade,” where lenders start sweating and clutching their pearls.

IREN itself is nowhere near an A. But the lenders aren’t betting on IREN-they’re betting on Microsoft, who enjoys a AAA rating, the financial equivalent of being knighted by the Queen. Because the debt is secured by Microsoft’s contracted payments, the agencies graded the strength of Microsoft’s promise rather than IREN’s balance sheet. In short, IREN borrowed against Microsoft’s reputation, which is a clever trick if you can manage it.

The one‑notch drop from AAA to A reflects the agencies’ mild discomfort with fast‑aging GPUs and the possibility that IREN might trip over its own shoelaces.

Why that rating unlocks the cheapest money

An investment‑grade rating doesn’t just look pretty on a slide deck. It determines who is allowed to lend. The market IREN tapped is where insurers and pension funds stash their money-vast pools of capital guarded by rules that forbid them from touching anything below investment grade. They like their investments like they like their tea: steady, predictable, and unlikely to explode.

Clear the investment‑grade bar and you gain access to the cheapest capital available. Miss it, and you’re left with private‑credit funds charging rates that make payday lenders blush. Microsoft’s credit rating is the key to this kingdom.

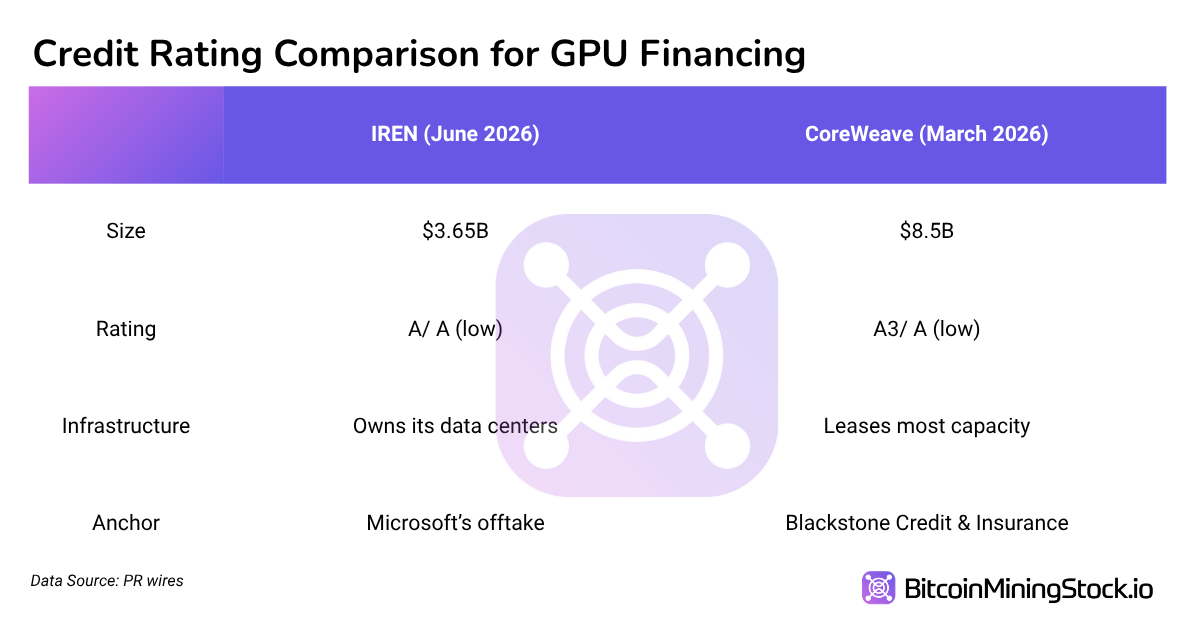

IREN isn’t the first

CoreWeave secured investment‑grade GPU financing in March, closing an $8.5B deal at a similar rating.

IREN’s rating is a notch higher, and it owns its data centers while CoreWeave mostly rents. You’d think that would earn cheaper money. It didn’t. Both priced around SOFR plus 2.13%. The real deciding factor wasn’t real estate or charm-it was the customer’s creditworthiness. Everything else was window dressing.

Final thoughts

So what should an IREN shareholder take from this?

The upside is undeniable. Funding a $5.81B buildout with debt and customer cash instead of issuing new shares is a refreshing reversal of the sector’s usual “dilute first, ask questions later” strategy.

The catch is leverage. Equity holders now sit behind lenders who have first claim on the GPUs and Microsoft payments. If the contract underperforms, shareholders may find themselves waiting politely at the back of the queue.

The broader rule is clear: what determines whether these companies can fund themselves cheaply isn’t their megawatts-it’s the credit rating of their customers. TeraWulf and Cipher have Google‑backed Fluidstack (Cipher also has AWS); Applied Digital, Core Scientific, and Hut 8 are chasing similar validation. Land an investment‑grade anchor, and you borrow like royalty. Fail, and you keep selling shares like a street vendor hawking trinkets.

Still, caution is warranted. GPUs age out in three to five years while the debt lingers longer, so the agencies are betting the contracts outlive the hardware. And much of this demand is hyperscalers funding the very capacity they intend to rent. It works-for now. But before buying any of these names, ask the question IREN just answered: who’s their customer, and how good is their credit?

Read More

- USD PHP PREDICTION

- Gold Rate Forecast

- Brent Oil Forecast

- USD CNY PREDICTION

- EUR CNY PREDICTION

- USD MXN PREDICTION

- Senate’s CLARITY Act: A July 4th Fireworks Display or Political Fire Sale?

- GBP CNY PREDICTION

- CNY JPY PREDICTION

- CNY RUB PREDICTION

2026-06-15 10:59